Global economic outlook more optimistic

What does that mean for Canada's outlook?

In its most recent global forecast, the International Monetary Fund thinks that most major economies will be able to avoid a recession this year, with average global growth expected to come in at 2.9%. The biggest change in their January forecast is a pretty dramatically improved economic outlook for Russia, and a moderately improved outlook for China.

Forecasts should always be taken with a grain of salt, they make assumptions about risks, and especially now some of those risks are pretty unpredictable. For people in the Euro area, 2023 is likely to feel pretty recession-y, whether it technically is defined as one or not.

This forecast also assumes that the US economy manages a soft landing. Today the US Fed announced its smallest rate increase yet, 25 basis points (0.25 percentage points), but they’re still worried about the strength of the labour market.

Part of the problem that the Fed faces is that investors are optimistic, and this works against the Fed’s attempt to make borrowing more expensive. Corporate bond yields are an indicator of how expensive borrowing is for major corporations. Even though the Federal Reserve has continued to increase their rates, yields of corporate bonds peaked near the end of October and have started to fall. Falling yields mean cheaper borrowing for corporations.

The average rate on a 30 year fixed rate mortgage in the US has also fallen from a high of 7.08% in the middle of November 2022 to 6.13% at the end of January 2023 (Source: Freddie Mac).

It’s clear that markets don’t believe the Federal Reserve. Maybe ‘the market’ is right, and inflation is mostly behind us. The Fed is still worried, and made it clear that they a) plan to keep raising rates, b) will keep reducing the size of their balance sheet (otherwise known as quantitative tightening), and c) have no intention of cutting rates before the end of the year. If ‘the market’ continues to blatantly disregard the narrative being put forward by the Fed, and inflation comes down too slowly for their comfort, the Fed may feel they need to be much more forceful in future meetings.

But who knows, we could be on that narrow path to a soft landing here. Paul Krugman wrote in the NYTimes today that he thinks that Larry Summers et al will have to concede they were wrong, and that ‘Team Soft Landing’ was right. I think it’s too early to tell.

What does it mean for Canada?

A soft landing in the US would be great news for Canada, since our economy is heavily dependent on theirs. This is especially true for Ontario, which was overly reliant on the real estate sector for pre-pandemic economic growth.

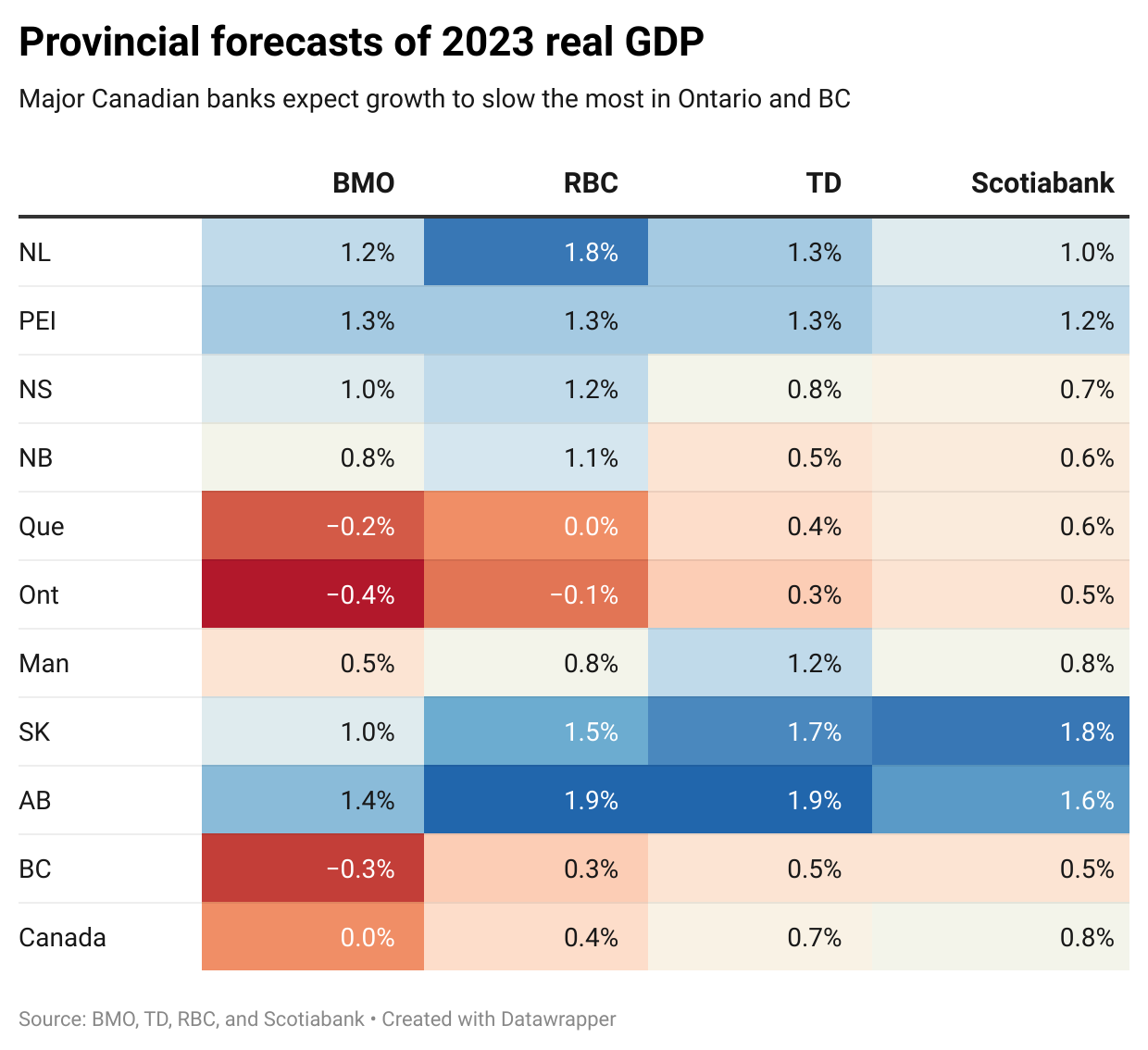

Major Canadian banks are less optimistic about Canada’s prospects for real GDP growth than the IMF. BMO’s January 6th forecast shows real GDP falling for Quebec, Ontario and BC this year, and average Canadian growth for the year flat. RBC’s forecast from December is slightly more optimistic, but it also predicts real GDP will shrink in Ontario this year. The Scotiabank and TD forecasts from December are also more optimistic than BMO, but are significantly lower than the IMF’s sunny outlook of 1.5% real GDP growth.

I’m inclined to agree with the big banks (I don’t say that often). Preliminary data from Statistics Canada shows that real GDP was flat in December, following two months of 0.1% increases in October and November.

The construction sector was the biggest drag on growth in November (seasonally adjusted), contracting in all but one sub-sector. The biggest contraction was in residential building construction - exactly the thing we desperately need more of. The construction sector can be an early indicator of broader economic trends, so that doesn’t bode well for 2023.

And as Jim Stanford has pointed out in this excellent post at the Centre for Future Work, even though real GDP was positive in the 3rd quarter of 2022, real final domestic demand was negative. This means that falling imports and rising exports (counted in GDP but not final domestic demand) carried us through that quarter. And rising inventories supported real GDP numbers in the 2nd and 3rd quarters of 2022, all signs of growing economic weakness under the surface.

The final ‘Canadian angle’ is that while our economy will likely continue to be supported by higher resource revenues in AB, SK and maybe NL, we are at risk of losing out from shifts in US and EU industrial policies. Friend-shoring aside, what the US really wants to do is support domestic industries, and the EU (especially France and Germany) are feeling pressure to do the same. If all Canada can bring to the table is more stuff we dig out of the ground (found on indigenous lands, no less), that’s bad news for both short term and long term economic growth, let alone ‘shared prosperity’.