On Recessions and Soft Landings

Economic forecasters are predicting low to zero economic growth for Canada (and the world) in 2023. What does that mean for us?

When central bankers raise interest rates as they have been, it almost always causes a recession. As the BoC was raising interest rates this summer, CCPA economist David MacDonald looked at its track record. He found three examples of headline inflation coming down by 5.7 percentage points (the amount of the reduction the BoC was looking for as of May), and each time was followed by a recession - in the mid ‘70s, early ‘80s and early ‘90s.

Many have been advocating for approaches that might mitigate the risk of recession (using a higher inflation target of 3% or 4%, for example), but central banks have been pretty clear that they think their credibility relies on getting to 2%, and fast.

Maybe this time will be different, but there has been widespread skepticism that a soft-landing is possible using the current approach of central banks.

The question on the minds of most economy-watchers has not been *if* there’s going to be a recession, but when and how bad.

Most people are familiar with the common ground rule that we’re in a recession if economic growth falls for two consecutive quarters. In Canada and the US, the way recessions are determined is a bit fuzzier - a group of economists look at economic data, and evaluate how long economic activity has been contracting, how deep the contraction is, and how widespread it is across different industries. Even though the US had two quarters of negative GDP growth in the first half of 2022, it wasn’t called a recession by the National Bureau of Economic Research (NBER) because the contraction wasn’t that deep and employment remained strong.

In Canada, the CD Howe Business Cycle Council determines when a recession started or ended, and they look for a “a pronounced, persistent, and pervasive decline in aggregate economic activity” to declare a recession. They use a scale of 1 to 5 to indicate the severity of the recession, with 5 being the most severe. Forecasters at major Canadian banks are predicting that Canada will have a relatively mild recession, with negative economic growth for at least the first two quarters of 2023, and unemployment rising from the current five percent into the mid-6% range.

Risks to the best case scenario

The best case scenario right now is that inflation continues to fall, and central banks stop increasing interest rates. We might get two quarters of falling GDP in 2023 as the impact of higher rates show up in business decisions, but employment remains mostly unchanged and overall growth quickly recovers.

This scenario is possible, but unlikely. A large part of falling inflation to this point can be attributed to easing pressures in global supply chains and falling oil and gas prices. We might not be getting much more help on this front any time soon.

The New York Federal Reserve has developed an index that tracks global supply chain pressures, called the GSCPI. This measure shows pressures have eased significantly from their peak in January 2022, but have stopped short of returning to pre-pandemic levels.

Canada’s Western Canadian Select (WCS) crude oil price peaked in June 2022 at $101 US/bbl, and was down to $57US/bbl in November. But that’s still higher than its 2019 average price of $44 US/bbl. This is a pattern similar to other global crude oil prices.

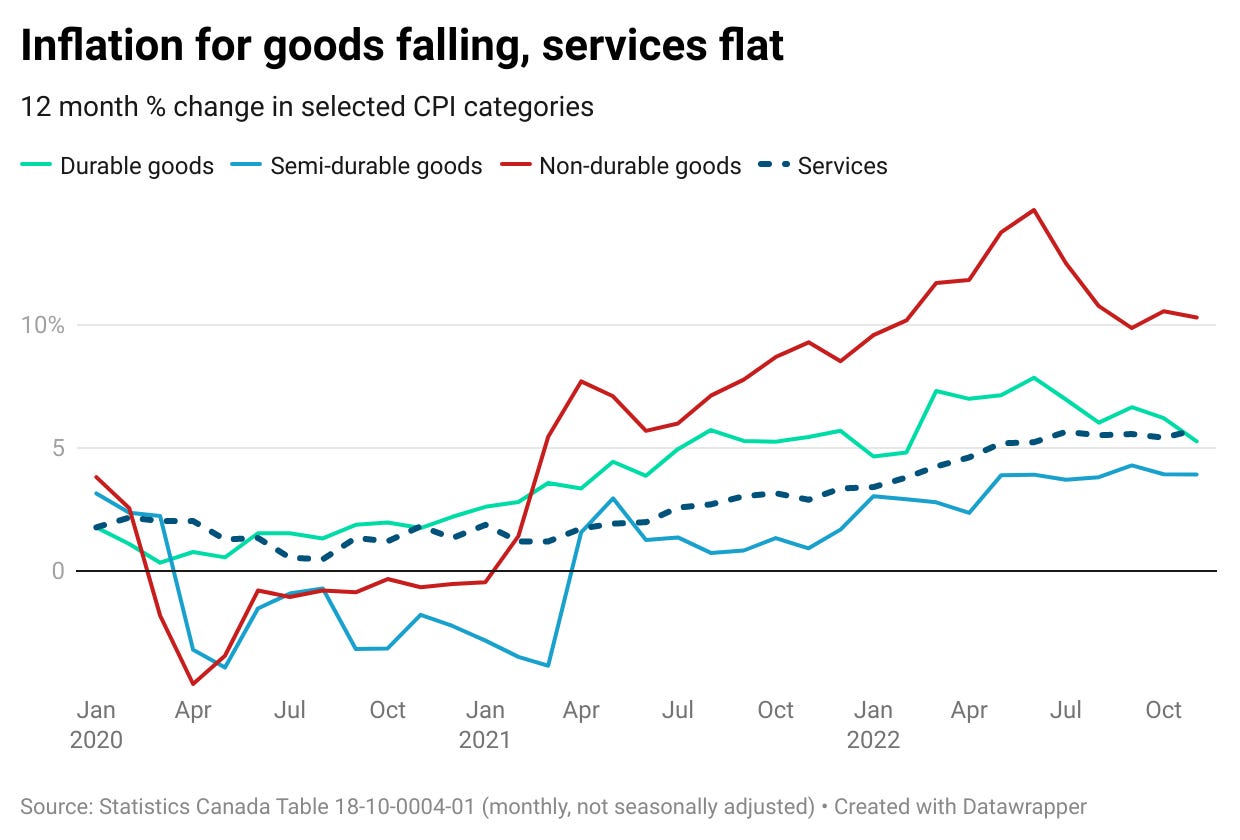

We can split CPI out into goods and services, and we see price pressures are easing for goods, but services have largely plateaued. Food purchased from stores falls under non-durable goods, and those prices have been increasing even as other components of non-durable goods have eased. Services price growth has slowed, but it’s still going in the wrong direction.

A similar dynamic is happening in United States, and this is why the US Federal Reserve has said that it’s paying very close attention to the core services component of inflation in their analysis. They separate services into housing and other services, which I have not figured out how to do for Canadian data yet. Pulling out housing services helps to remove the impact that higher interest rates have on inflation.

A focus on services inflation is bad for workers, but also for the chances of a soft landing. Workers wages make up a bigger component of the the cost of delivering services, and it’s easier to make the case that overall demand growth (think employment * average compensation) is a larger factor in price growth for services than it is for goods. As long as employment remains strong, central banks will see that as a risk to inflation falling.

If central banks only think their plan is working when unemployment goes up, then they’ll keep raising rates until that happens (or inflation goes away). Unemployment is at record lows right now, and inflation doesn’t look like it will immediately disappear on its own. So I’d bet on getting a recession in 2023, with the severity depending on how impatient the Bank of Canada is to dampen wages and employment.

Low inflation isn’t the bedrock of a healthy economy

I’m a huge fan of Claudia Sahm, not just for her analysis but also for her vocal advocacy around improving the economics profession for women and racialized people. Her analysis here is bang-on:

The benefits of low inflation exist for consumers, but they come at a cost to workers. Most Americans are consumers and workers; low wage growth offsets benefits from low inflation. For shareholders and the C-suite low inflation world is a win-win. But the 1%, as with the Fed, is not the economy.